How to Implement AI in a PE-Backed Services Business

MAY 2026

"There are many papers on the importance of AI covering trends and theories. This one gets into tangible examples of what AI can do in a real company and what operators can actually do if they want to help implement AI in portcos. It is excellent."

Contents

What's inside

- —Executive Summary

- 01The AI OpportunityThe PE risk framework.

- 02Knowing About AI Is Not the Same as Implementing ItThe paradox and the trap. The AI Transformation Model.

- 03Three Types of Value, with Real ExamplesReplace, Expand, Invent.

- 04The Tech Stack Required to Actually Build ThisThe three-layer architecture & agent governance.

- 05aHow to Implement This AI StackThe four phases. Tracking adoption.

- 05bThe New Support EcosystemBuy or build is no longer the question.

- 06The P&L and Valuation ImpactTokenomics, headcount, and the biggest fault line in PE valuations.

- 07Due DiligenceThe six questions.

- 08The Cost of Waiting

Executive Summary

Most AI white papers tell you AI is disruptive and leave you with talking points. This one contains the operating playbook.

I have spent the last year rebuilding a 1,000-person company around AI. Below I document the architecture, the implementation detail, and the operating metrics from that process. Not just theory, but actual systems, what it cost, how it was built, where we went wrong, and what it can currently produce.

What this paper covers

Section 01: The AI opportunity. The data is unambiguous: AI creates more enterprise value than any operational lever in a generation. The automation potential is larger than previously understood, and the divergence between leaders and laggards is accelerating. You probably already know this, so feel free to skip to Section 02.

Section 02: Knowing about AI is not the same as implementing it. 78% of deployments produce no P&L impact, because companies are layering AI onto existing processes instead of redesigning around it. Notion's AI Transformation Model places 80% of companies at Level 1. Fewer than 2% reach Level 4. This paper is written from the perspective of a Level 4 company.

Section 03: Three types of value, with real examples. Replace (existing tasks done by AI instead of people), Expand (existing tasks done more often or taken further), and Invent (previously unachievable work). The examples are not jaw-dropping individually. That is the point. AI value comes from volume and compounding, not from any single spectacular use case. Each type comes with specific workflows running in production today.

Section 04: The tech stack. An AI-native company runs on three layers: a data layer, a logic layer (the brain, where agent instructions and governance live), and an execution layer (where AI agents take action). This section explains our tech selection for each, how each layer works and how they connect.

Section 05a: How to implement it internally. Four parts: decide who leads, organize the data layer, roll out training and measurement, and continue integrating. Plus the adoption dashboard that tracks whether any of it is working. Includes real but anonymized data from 850 users across 18 functions.

Section 05b: The new support ecosystem. The old "buy or build" question is dead. AI has created a third option: neither pure technology nor traditional consulting, but practitioners who understand real business challenges building AI agents to solve them. This section covers the structural break, the growing implementation market, and some initial ideas on how PE sponsors can orchestrate AI transformation across an entire portfolio simultaneously.

Section 06: The P&L and valuation impact. Token economics and what it actually costs to run AI agents at scale. What happens to headcount. Early operating data from a production deployment. Then the valuation side: the widening fault line between AI-ready and AI-absent companies in PE portfolios, Canaccord Genuity's M&A deal sheet as a live index of where AI value is being created, and AI readiness as a multiple enhancer at exit.

Sections 07–08: Due diligence and the cost of waiting. Six questions every GP can ask. Then the compounding cost of delay during a hold period. The companies that moved in 2024 and 2025 are pulling away. The gap is not linear.

Section 01

The AI Opportunity

You already know this is big. Here is why it is urgent — the biggest operational lever PE has seen in a generation, and the evidence behind it.

You would not have opened a paper called "How to Implement AI in a PE-Backed Services Business" if you needed convincing that AI matters. So this section is short.

The headline numbers, for reference: generative AI could add $2.6 to $4.4 trillion in annual economic value globally, with 75% concentrating in customer operations, marketing and sales, software engineering, and R&D.1 Automation potential has jumped to 60–70% of work activities, up from the prior 50% estimate, and McKinsey's midpoint for when half of all work could be automated moved forward a full decade.1

The gap between companies that act and companies that wait is already visible in the data. BCG's research shows that the top 5% of companies are generating significantly higher returns than their peers:2

The PE risk framework

Sanjay Chadda at Canaccord Genuity has advised on over a dozen AI-related transactions in the past 24 months. He sees the bifurcation from the deal table:

"AI-enabled companies with defensible positions command premiums, while businesses without a credible AI strategy face lower multiples and fewer interested buyers. The due diligence exercise has fundamentally changed, as sponsors are evaluating AI substitution risk alongside traditional metrics."

Sanjay ChaddaCanaccord GenuityNick Bueno at Falfurrias Capital Partners breaks AI risk at the portfolio level into two categories.12 The first is substitution risk: the probability that AI can replace the core work a company does. If a business sells a service that AI can now perform at lower cost and higher speed, the value of that business is under direct pressure. The second is ecosystem risk: even if your company is not directly substitutable, your clients, suppliers, competitors, or end-users further down the value chain are changing how they operate because of AI. If your customers are adopting AI and your company cannot plug into their new workflows, you become friction in their system. Both risks need separate assessment, and both need honest answers.

Bueno sees the impact playing out as a bimodal distribution across services businesses with knowledge-work-heavy workflows. AI's impact is not incremental. It is binary. Some companies will see game-changing results. Others will see nothing. There is no smooth curve where everyone gets a little benefit. The determining factor is whether the company actually rewired how it works, or just bought tools and added them to existing processes. For PE, this means the spread in outcomes across a portfolio will be wider than any previous technology cycle.12

The technology itself is accelerating faster than many PE sponsors appreciate. AI task completion rates are doubling every seven months.9 The models released in early 2026 crossed a threshold: they iterate on their own work, test their own outputs, and refine until they are satisfied. The current generation already does this today.

Section 02

Knowing About AI Is Not the Same as Implementing It

Where companies actually sit on the adoption curve, and why most are stuck.

Here is the paradox: 78% of organizations have deployed gen AI in at least one function, yet the same 78% report no significant P&L impact. Only 1% describe their deployments as mature. Fewer than 10% of use cases have made it past the pilot stage.3

The reason is simple. Companies are layering AI onto existing processes instead of redesigning processes around AI capabilities. A pilot needs a dataset, an API key, and a willing team. Production needs data governance, security architecture, integration with existing systems, change management, and organisational redesign. Sixty percent of companies cannot even define financial KPIs for their AI investments.5 Without measurement, there is no way to distinguish a successful experiment from an expensive hobby.

A note on what the consultancies can and cannot tell you: McKinsey, BCG, and Bain are excellent at sizing opportunities and identifying trends. Their data is rigorous and directionally correct. Where they are weaker is on the question that matters most to an operating partner: what do I actually do about this? The technology is too new for anyone to have a tested, proven playbook. The models that make agentic AI possible shipped months ago, not years ago. Anyone selling you a mature implementation framework for something this new is ahead of the evidence. The rest of this paper is an attempt to fill that gap with what we have actually built and tested. It is not complete, but it is real.

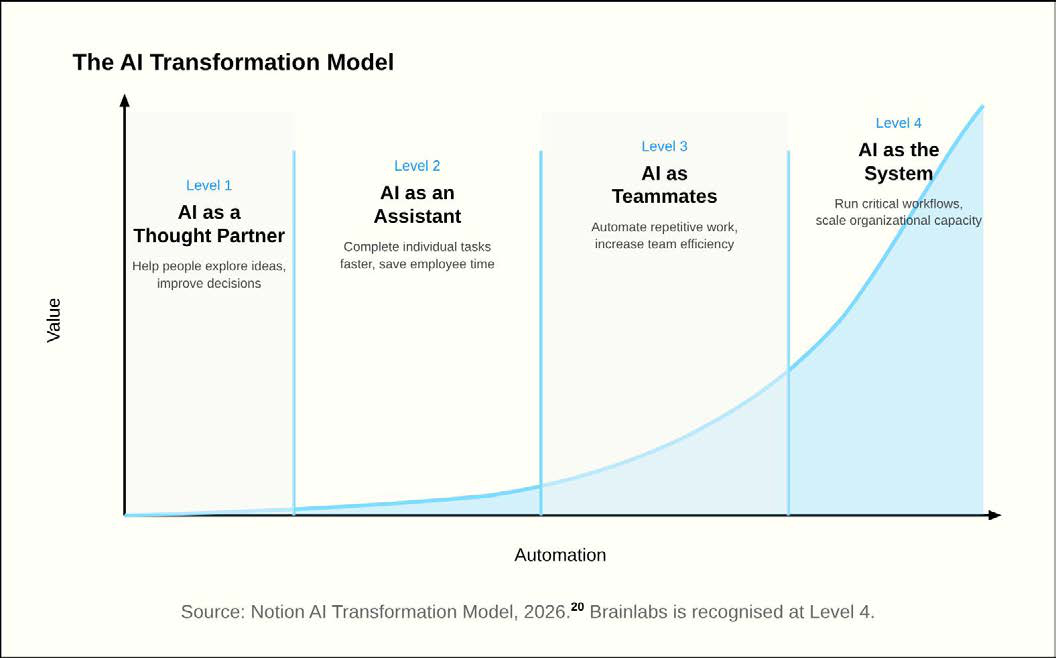

The AI Transformation Model

Notion is the AI workspace platform behind over 100 million users and more than half the Fortune 500, and one of the fastest-growing AI enterprise software companies of the last decade. Their AI Transformation Model maps four levels of AI maturity drawn from real company journeys, created in partnership with Ben Levick (Head of AI & Ops at Ramp), Geoffrey Litt (Author, MIT researcher, Engineer at Notion), and others.10

Individuals using AI ad hoc. Chatbots, prompts, single-player productivity.

Context-aware AI embedded in daily work: meeting notes, search, document drafting. Measurable time savings, but still assistant-level.

AI agents handling recurring workflows end to end. A team-level operating system. Companies here reclaim 10–40% of team capacity.

Multi-agent orchestration, proactive and self-improving workflows, policy and governance built in. Brainlabs is recognised at this level.10

Section 03

Three Types of Value, with Real Examples

Replace, Expand, Invent. Three categories, with worked examples from production.

Before reading the examples below, a word on expectations. None of this will feel like science fiction. The calculator did not introduce a new type of math. The typewriter did not enable a new type of prose. AI, at its core, is a large language model: it predicts what comes next, very fast, very often, across very large amounts of information. David Deutsch makes the point that genuine novelty in knowledge creation is rare and hard to recognize. Most progress comes from applying known methods at a speed or scale that was previously impractical. The individual examples are mundane on purpose. A report gets written. A budget gets paced. An audience gets segmented. The difference is that all of it now happens continuously, across every function, with minimal human bottleneck. It is the volume that changes the game, not magic.

We categorize AI value creation into three buckets, each with distinct timelines and value potential. What follows fills each bucket with actual workflows running in production at Brainlabs today. Not theoretical use cases. Real work, done by real people, with measured results.

Apply AI to current processes. The fastest path to value but also the shallowest. The work stays the same; AI just does it faster.

Create entirely new capabilities enabled by AI. Things the company could not do before, not because it lacked ideas, but because the execution was too expensive or too slow.

BCG's data shows that companies achieving "future-built" status are deploying AI in 9–12 months versus 12–18 months for the rest, and 70% of their AI value comes from core business functions rather than peripheral experiments.2 The rest of this section shows what each horizon looks like in practice, with one worked example per bucket followed by a sample from the hundreds of other agents in production.

Bucket 1: Replace. Do what you already do, faster.

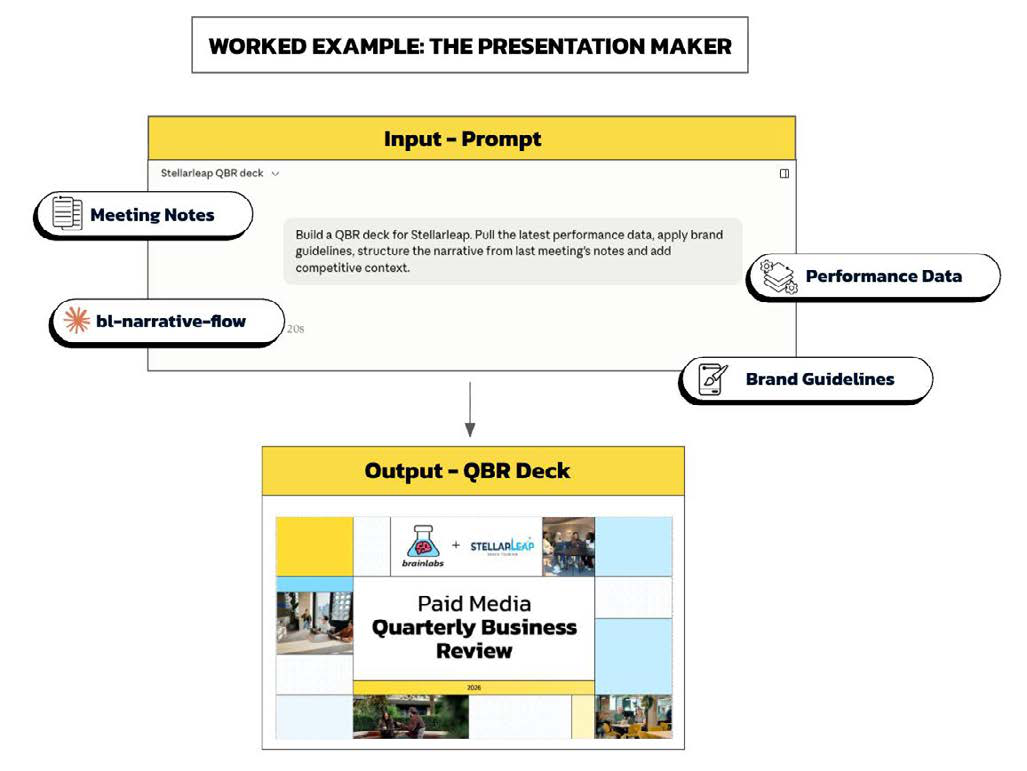

Every services company makes presentations. At Brainlabs, creating a typical quarterly business review deck used to take a full day or two. The work got divided across a team: one person pulling data, another writing the narrative, someone else formatting slides, a fourth adding competitor context. Coordinating that team meant chasing availability, dealing with out-of-office messages, version-merging three different drafts, and the inevitable "can you just tweak slide 14" round-trip. The total cost was about 10–20 hours of people-time per deck.

Now, a single person opens Claude Cowork, triggers the presentation agent, and the system pulls data from live dashboards, applies the brand guidelines, structures a narrative from meeting notes and performance data, and produces a formatted deck. Total time: about an hour, most of which is the human reviewing and sharpening the output. That is 10–20 hours of people-time back per deck. The person who used to coordinate the whole process can spend that day on strategy instead of adjusting slides and coordinating a team.

That is one agent out of hundreds. Below is a random sample of other Replace workflows running in production. The point is not these specific examples. It is that there are hundreds more like them, across every function in the business, even HR.

| Agent name | Description | Before | After | Saving |

|---|---|---|---|---|

| market-intelligence-report | Produce a comprehensive market intelligence report for a new region | 2 weeks | 30 mins | ~99% |

| legal-msa-client-paper-redliner | Redline a client MSA against our playbook and flag risk areas | 8 hrs | 15 mins | ~97% |

| newbusiness-final-submission-review | Review and QA an RFI response document before client submission | 6 hrs | 15 mins | ~96% |

| paidsearch-ad-copy-refresh-builder | Build a full ad copy refresh deliverable from Google Ads data | 8 hrs | 30 mins | ~94% |

| multichannel-performance-report | Generate a weekly client performance newsletter from campaign data | 4+ hrs | 15 mins | ~94% |

| programmatic-client-report-qa | QA and build a weekly client monitoring deck from platform data | 3+ hrs | 15 mins | ~92% |

| retail-media-pacvue-negative-keyword-analyser | Build negative keyword lists from Pacvue search term reports | 3 hrs 30 mins | 15 mins | ~93% |

| seo-post-meeting-processor | Process meeting transcript into action items, notes, and follow-ups | 1 hr | 5 mins | ~92% |

The same pattern shows up in client delivery, not just internal operations. One client, a real estate company, manages over 500 properties, each running daily promotions. Previously, a team member had to read each emailed promo description, interpret the offer, classify it, and manually implement the changes in Google Ads — around 20 promotions per day, each taking several minutes, with a 2–3 day turnaround. Now an AI agent reads the email, classifies the promotion type, and implements it in the ad platform automatically. The team's role shifted from doing to QA-ing. Turnaround dropped to under 24 hours.

A global hospitality brand with 100+ premium properties needed bi-weekly, property-level campaign insights across its entire portfolio. The process consumed up to three days of team time. An automated system now pulls the data, generates the insights with industry context, and presents them in a single dashboard. Three days became one.

These are not internal experiments. They are running in production, on real client accounts, handling real money. The pattern is always the same: AI does the first pass, humans verify and sharpen. The economics flip from "person does work, machine assists" to "machine does work, person approves."

Bucket 2: Expand. Increase frequency and scope.

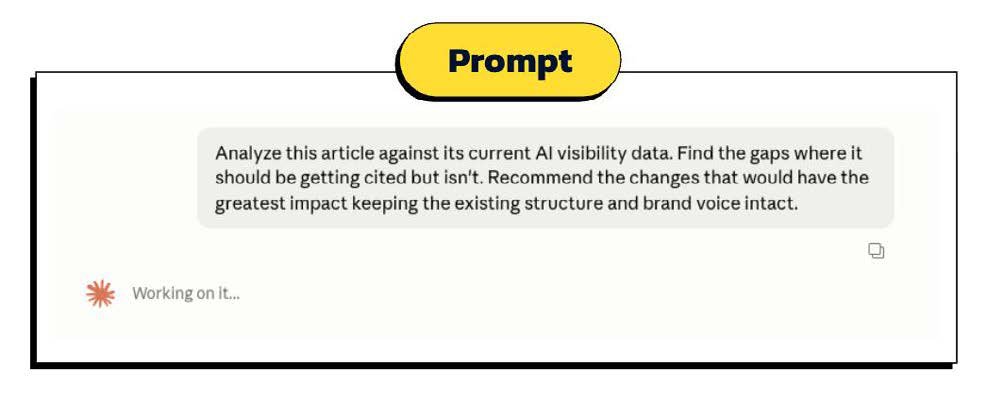

Brainlabs is a marketing agency. One of our core services is AI Visibility: getting clients mentioned, recommended and trusted in AI-generated answers. Part of that work is regularly refreshing content on their website, because AI systems are more likely to cite pages that have been recently updated. The refresh entails identifying which pages have fallen behind, sourcing current data, restructuring content for how AI actually reads, and rewriting to close the citation gap. The problem was never whether doing that was worth it. The problem was capacity. It would take a senior practitioner about half a day per page. With clients holding hundreds of indexed pages, only the top few ever got a refresh, and only once a quarter.

Before

- Frequency

- Manual audit triggers a refresh. Smaller pages never get one.

- Coverage

- Top 20 pages per client.

- Detail

- When a traffic drop became hard to ignore.

After

- Frequency

- Continuous monitoring.

- Coverage

- Full content library.

- Detail

- Agent monitors ranking signals and AI citation gaps; practitioner reviews and approves rewrites.

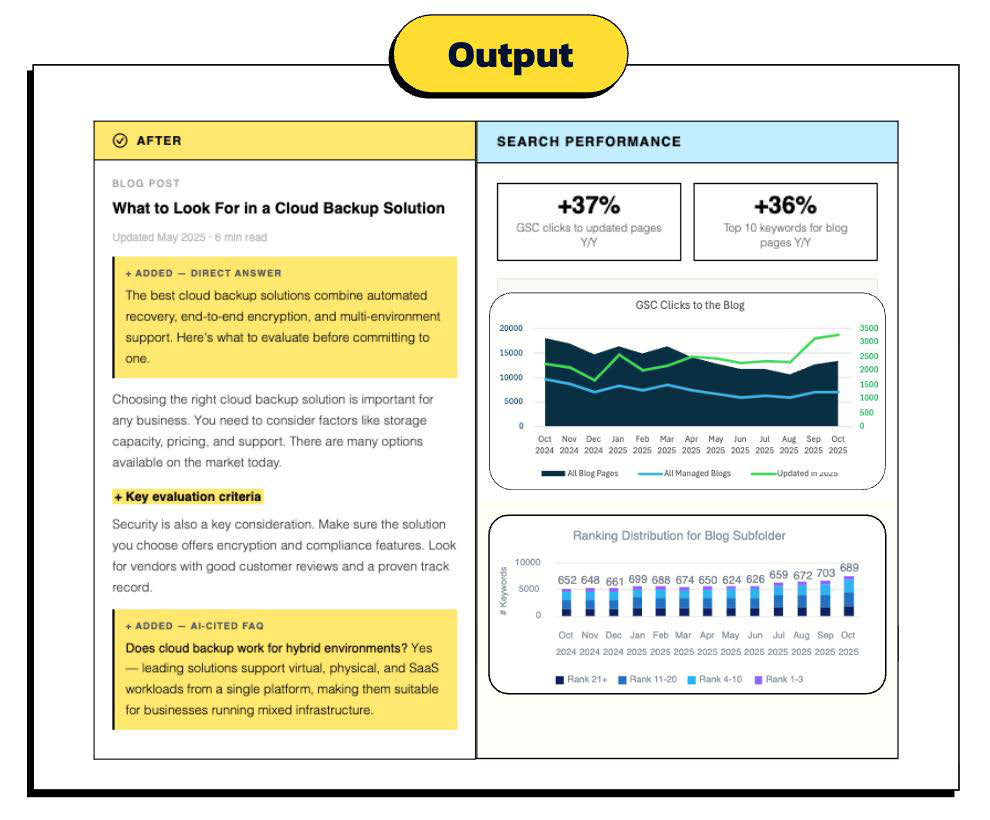

Now an agent tracks the full content library for every client, every week. It monitors which pages are losing citation ground to competitors and flags the keywords where the client should own the AI answer but doesn't. It identifies the structural and factual gaps on each page, then drafts a full refresh: updated statistics, new examples, restructured headers, tighter definitions. The practitioner reviews and approves. The result is not faster refreshes. It is a fundamentally different cadence: work that happened for five pages a quarter now happens for every page, every week.

One enterprise software business saw a 37% increase in clicks and a 36% growth in top-10 keyword rankings on pages they had created last year. AI Overviews have already driven a 30% decrease in clicks from traditional search results. Seventy-three percent of consumers who use AI for shopping cite it as their primary source of product research. A brand not cited in those answers has not just lost a ranking. It was never in the conversation.

Expand is where the majority of value lives because it changes what the company can offer, not just how fast it delivers. Below is a random sample from the workflows that fit this bucket.

| Agent name | What it does | Why it happened rarely | What changed |

|---|---|---|---|

| gmp-gtm-cleanup-analyser | Full GTM container audit and cleanup plan | Took multiple days; always deprioritised | Now feasible to run for every container |

| newbusiness-brief-intelligence-dashboard | Full pitch intelligence dashboard | 2–4 hours of manual research per pitch | Now runs for every pitch, not just the big ones |

| seo-aio-citation-checker | AI Overview citation tracking across keyword sets | 5.5 hours per analysis; priority clients only | Now scalable across every client and market |

| assessment-centre-grader | Assessment centre grading | 15–30 mins per candidate, manually | Every submission graded instantly at scale |

| deploy-html-to-google-sites | Internal deployment platform for tools and pages | Required a developer and a support ticket | Any employee can build and ship a live website from a conversation |

| social-product-mockup | Social product mockups for client presentations | 5 hours per mockup; rarely justified | Now routine for every client presentation |

"This replaces time tracking. I don't care about hours. I care about output. The system tracks output across all platforms without surveillance."

Daniel Gilberton the automated weekly summaryBucket 3: Invent. Do work that was not possible before.

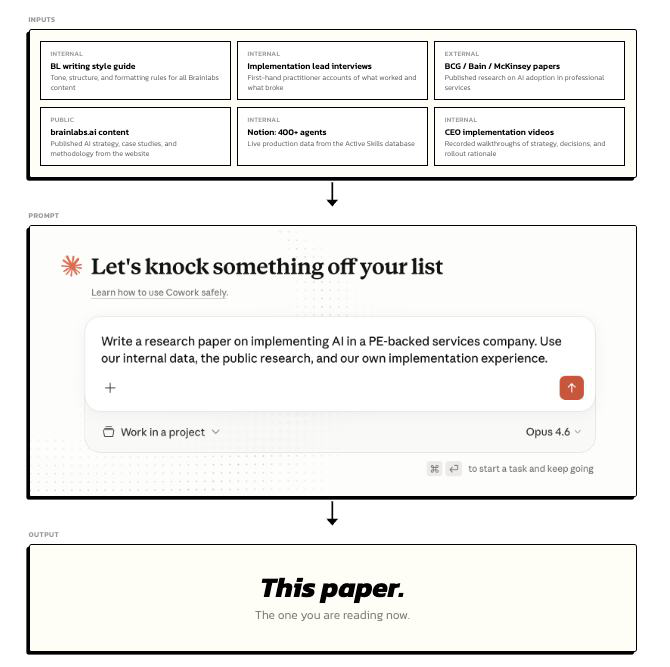

This very paper you are reading at this precise moment fits in Bucket 3, because it is not about time saved. It is a live example of work that would not have existed at all before our AI transformation.

I am the CEO of a company in the middle of implementing AI across 1,000 people. I do not usually have time to write research papers. If a consultancy wanted to produce a paper like this, they would spend months on it: a research team, analysts, writers, designers, partners reviewing drafts, compliance checks, a market study group running the numbers. It would cost six figures and take a quarter. We were never going to commission that. So this paper simply would not exist.

Instead, I built it in an afternoon. I have barely typed a single word. Our AI stack helped me pull in real internal data (our data warehouse, agents database, adoption dashboards, infrastructure documentation), combined it with external research, collated some other articles and posts I'd published, applied my impeccable writing style, and produced what you are reading this very moment. It did take lots of back and forth with verbal feedback, dictated to Claude through WisprFlow. I spent almost all my input time on judgment: which arguments to make, which examples to feature, what to cut. The machine did the perspiration while I did the inspiration.

The value here is not capturable as simple "hours saved." I was never going to write this paper in a previous working world. The value is that it exists, you are currently reading it and thinking that Brainlabs must be an amazing marketing agency. Maybe it convinces you that your portfolio companies should be thinking about AI differently. Maybe it leads to a conversation about switching their marketing agency to Brainlabs. Maybe it leads to you buying my company for billions. Actually that would be great, thank you for your prompt attention to this matter.

Anyway, the ROI is unknowable in advance, which is exactly what makes it Bucket 3: new output with new upside that could not have been justified under the old cost structure.

Scale that across an organization. We have over 400 agents in production covering every practice area: paid search, paid social, SEO, CRO, programmatic, influencer, client leadership, new business, finance, people operations, and IT. The people who do the work built each agent, tested it against real outputs, and improved it through a governance process where any employee can submit updates.

The three buckets are not a maturity sequence. They run in parallel. Most companies start with Replace because it is the easiest to measure, but the real value accumulates in Expand and Invent.

Section 04

The Tech Stack Required to Actually Build This

The three-layer system that makes Section 03 possible, and how agents are captured, governed, and scaled.

Section 03 showed the outputs. This section explains what makes them possible. The architecture has three layers, and each one is necessary.

A quick guide to the jargon

- Agent

- A reusable AI workflow, written in plain English, that tells the AI exactly how to complete a specific task. It can read data, call APIs, send messages, create documents, and complete multi-step workflows. Think of it as codified expertise that takes actions, not just answers questions. Anyone can invoke an agent. The AI follows the instructions. The person applies judgment to the output.

- Context window

- The amount of information an AI can hold in working memory during a single interaction. The quality of AI output depends directly on how much relevant context it has. This is why a structured knowledge base matters: it feeds the AI the right context at the right time.

- Wrapper

- The software layer around the AI model that gives it memory, file access, tool connections, and the ability to act. Claude's wrapper tools (Cowork for non-technical users, Code for developers) are what turn a chatbot into a working system.

The three-layer architecture

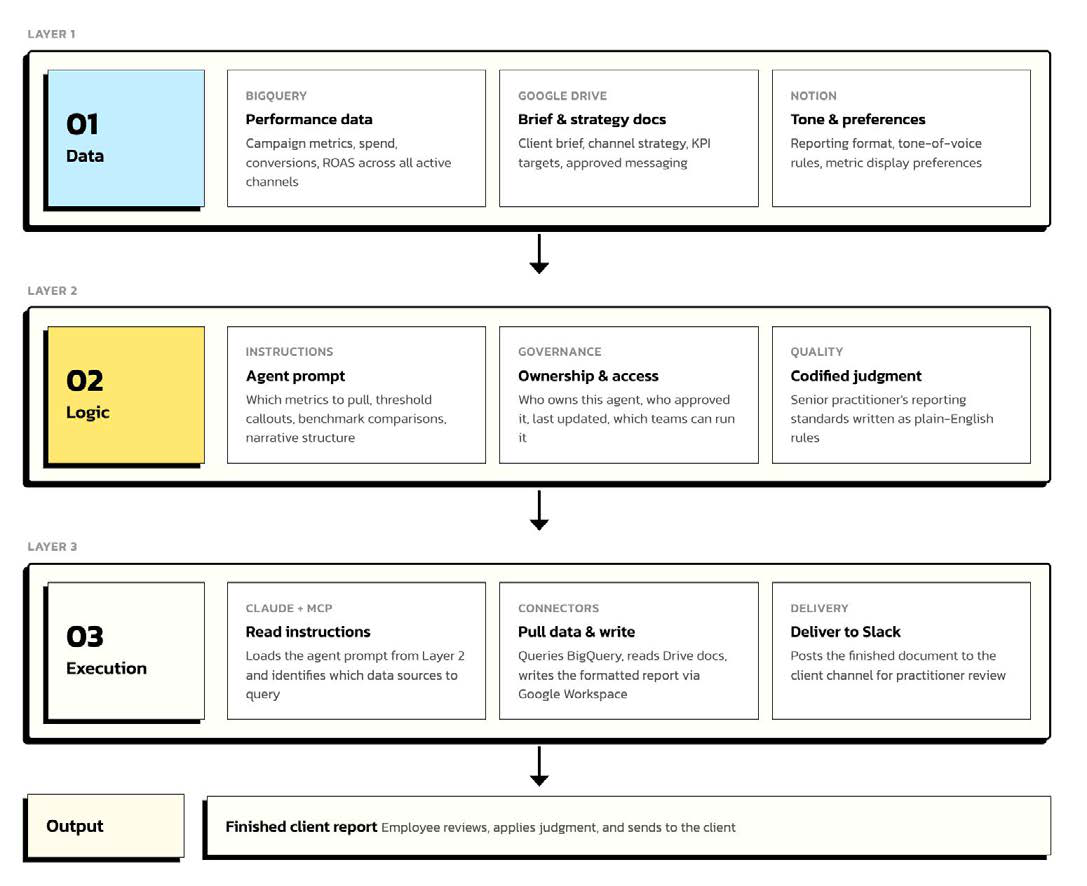

Layer 1: Data (Notion + BigQuery). This is where all of the information about the company lives. Every process, policy, client brief, piece of institutional knowledge, and performance dataset sits in a structured, searchable, machine-readable format. Notion holds the operational knowledge. BigQuery holds the data. Without this layer, AI has no context to work from and every interaction starts from zero. The AI reads them the way a new employee reads the company wiki, except it does it in milliseconds and never forgets.

Layer 2: Logic (Notion as the brain). This is where the agent instructions, logic, governance, and access control live. When a senior employee figures out the best way to write a client status report, prepare a QBR deck, or audit a search campaign, that process is codified as an agent and stored here. The logic layer defines what each agent does, who can use it, what quality standards apply, and how it connects to the data layer below. It is the institutional memory of the company, structured so that machines can read it and act on it.

Layer 3: Execution (Claude and AI agents). AI systems that sit on top of the first two layers and take action. Not chatbots that answer questions. Agents that complete tasks: drafting client reports, building campaign structures, preparing weekly updates, analyzing performance data. These agents read the data from Layer 1, follow the logic from Layer 2, and connect to Slack, Google Workspace, Google Drive, and the company's internal databases through standardized protocols (MCP, the Model Context Protocol), so they work with the same tools employees already use.

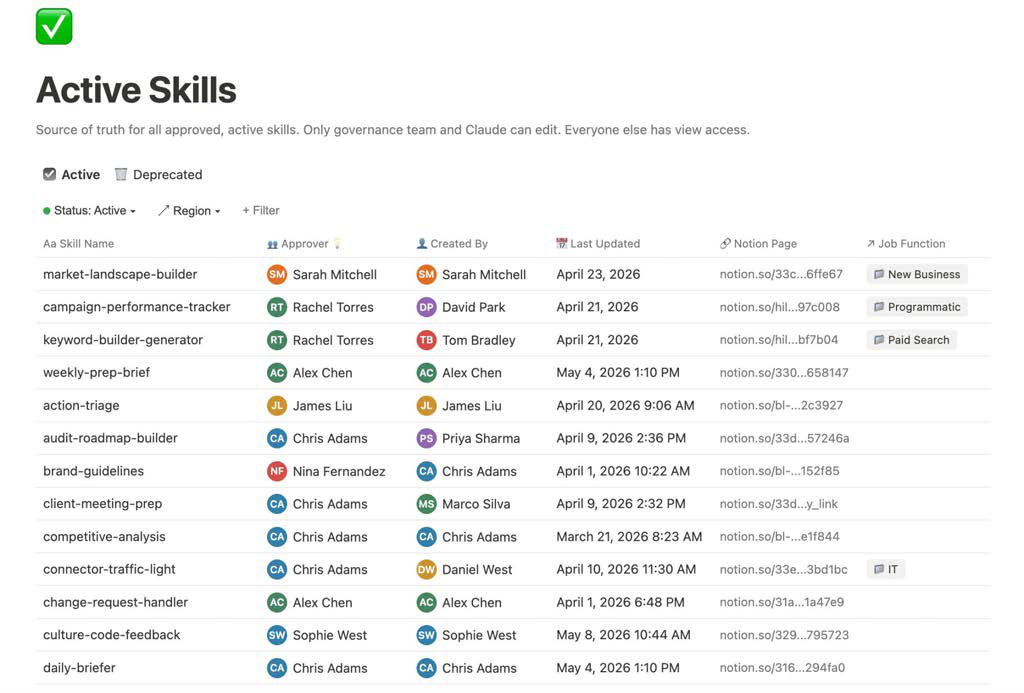

Visibility: every agent needs to be visible to everyone

In a serious company, you need to know what your AI is actually doing. That means a central library of every agent: what it does, who built it, how often it runs, and whether it has been reviewed. At Brainlabs, over 400 production agents span every function.

Agent governance: building a palace, not pitching tents

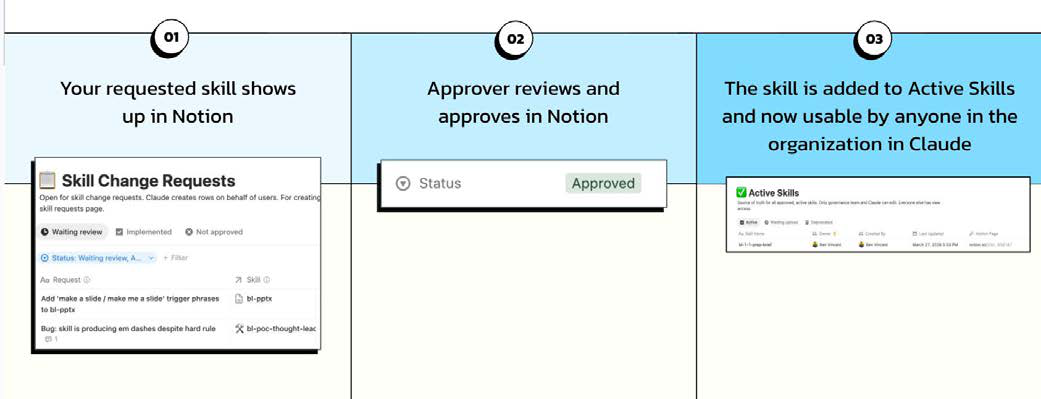

The biggest risk in any AI rollout is fragmentation. The real problem is people building their own agents on their own personal computers: plugging in a Mac Mini, running an open-source model, hardcoding passwords, creating automations that live on their laptop and nowhere else. Lots of individuals doing useful things for themselves, invisible to everyone else, gone the moment they leave or get promoted. Every one of those individual automations is a tent: useful for the person who pitched it, invisible from the outside, blown away in the first storm.

The alternative is shared infrastructure. When a senior person figures out the best way to write a client status report, that process becomes an agent. Any team member can invoke it. Every time someone improves an agent, every user of that agent benefits immediately. A junior account manager gets the same quality standards, the same analytical framework, and the same output format that the most experienced person on the team would produce. Institutional knowledge stops being trapped in individuals and becomes organizational infrastructure.

The governance works like this: any employee can submit a new agent or propose an update. A designated owner (usually the most senior person in that practice area) reviews and approves changes. Once approved, the agent is immediately available to everyone. This creates a flywheel: more people using agents means more feedback, which means better agents, which means more adoption. We have a leaderboard tracking who builds the most agents, who uses them most, and which agents save the most time. People want to be the person whose agent gets used thousands of times a month.

"We are building a palace, not pitching tents."

— me, just nowThen you need to build in Error Correction

In case any reader thinks this is all seamless: the first version of any agent rarely works well. Someone builds it, ships it, and the people who use it report what broke. The builder fixes it, ships again, and the cycle repeats. Our governance system formalizes this: every agent has an owner, every update goes through review, and the improvement history is logged. Over hundreds of iterations, the agents get genuinely good. Not because anyone designed the perfect version upfront, but because the system is built to catch and correct mistakes continuously. If that sounds like the scientific method applied to operations, it is. That was always the point.

We got plenty wrong along the way. Before we standardized on Claude, people across the company were using whichever LLM they preferred: Gemini, ChatGPT, Copilot, whatever they had tried first. The result was fragmented. No shared context, no shared agents, no way to build infrastructure that compounds. The decision to pick one platform and commit to it was painful but it was the single most important infrastructure decision we made. You cannot build a context layer on top of five different models.

How the three layers work together

Take the client report agent, one of over 400 in production. It exists in three places at once. In Layer 1 (Data), the agent has access to the client's performance data in BigQuery, their brief and strategy documents in Google Drive, and the team's tone-of-voice rules and reporting preferences stored in Notion. None of this was created for the AI. In Layer 2 (Logic), the agent's instructions live in Notion as a plain-English document: which metrics to pull, what thresholds trigger a callout, which benchmarks to compare against, the narrative structure of the report, and the client's preferred format. In Layer 3 (Execution), Claude reads the instructions from Layer 2, pulls the data from Layer 1, and connects to Slack, Google Workspace, and the company's internal databases through MCP. It writes the report, formats it, and delivers a finished document. The employee reviews, applies judgment, and sends.

The three layers are what separate this from someone using ChatGPT at their desk. Without Layer 1, the AI has no context. Without Layer 2, every person writes their own instructions and quality is inconsistent. Without Layer 3, the AI cannot take action on real systems. All three have to work together, and the architecture has to be deliberately built. That is why Section 03's outputs look mundane: the complexity is in the infrastructure, not the output.

Section 05a

How to Implement This AI Stack

Four phases. The sequence matters more than the speed.

There is no universal timeline. A 50-person company could move through these phases in weeks. A 5,000-person company might take a year. The sequence matters more than the speed.

Phase 1: Decide who is leading this

The single biggest risk in companies trying to go AI-native is that the person leading it does not actually understand the tools. They have what Charlie Munger called "chauffeur knowledge": they can repeat the talking points, but they cannot answer a question that was not in the script. You need what Max Planck had: real understanding earned through real practice.

Nick Bueno's view on ownership is specific: you need a senior owner who lives in the tools, with CEO sponsorship and active involvement. The CFO or P&L owner needs to be accountable for ROI on AI spend from day one. Not the CEO running every sprint, but the CEO visibly backing the initiative, removing blockers, and holding the organization accountable for adoption.12

I personally spent many 80-plus hour weeks learning the tools, making mistakes, killing failed approaches, and figuring out what actually works at scale. Leadership credibility on AI comes from whether you can sit next to someone, open the tools, and solve a problem together. Buying enterprise ChatGPT licenses and sending round a "tips for prompting" PDF is not a strategy.

We assembled a cross-functional team reporting to me to help with the rollout. We called it the Trio Model: every department gets a domain expert (the person who knows the work), a tools specialist (the person who knows how to build agents), and a technology specialist (the person who handles integrations and infrastructure). This gives every function the combination of knowledge it needs to move without waiting for a central team.

Phase 2: Organize the data layer

Garbage in, garbage out. The most important step in the entire process. The difference between a high-quality answer and a low-quality answer from an AI model is literally the context you provide it with. Before you can build anything, your company's knowledge needs to live somewhere structured and accessible.

Pick a single system of record. Everything: processes, client information, policies, playbooks. If your knowledge is scattered across drives, wikis, and people's heads, AI has nothing to work with. The unglamorous phase that most companies skip. Do not skip it.

We chose Notion as our system of record and Google BigQuery as our data warehouse. The reasoning was practical: Notion is structured enough for AI to read but flexible enough for humans to actually use it. Most enterprise knowledge management tools fail on one side or the other. Notion sits in the middle. Every piece of company knowledge lives in one place, structured with properties and relations that AI agents can query directly. BigQuery handles the quantitative side: performance data, financial metrics, operational analytics. Together, they form the data layer that everything else sits on top of.

Phase 3: Roll out, train, and measure

Our onboarding training was not a webinar and a tips document. We ran structured sessions across every region. Same format each time: the vision, the technical layer (what Claude is, how the tools work, what agents are), then straight into hands-on exercises. People built a working agent within the first hour. Safety training was built into the same session because separating "how to use it" from "how to use it responsibly" sends the wrong signal.

The facilitators were the people who built the system. Not external consultants. If someone hit a wall, the person helping them knew the answer because they designed the architecture.

Expect failures in Phase 3. They are the signal that the system is working. Our early agents were mediocre. Some were worse than that. But the architecture is designed so that every failure gets caught, reported, and fixed by the person closest to the work. The first version of a skill is a hypothesis. Usage data and user feedback are the experiment. The improved version is the result. Ship, test, fix, repeat. Companies that wait for perfect agents before deploying will wait forever.

Phase 4: Continue to integrate

This phase never ends. As people start using AI and seeing what it can do, demand for more connections grows. They want the AI hooked into the CRM, the project management system, the client platforms, the internal tools. Every new connection (an MCP, or Model Context Protocol) gives the AI access to another data source and another set of actions it can take. A compounding loop, not a go-live date. There is no finish line. The companies that move first will extend their advantage every month.

What this paper does not cover

Two risks deserve acknowledgment. The first is vendor concentration. We chose Claude as our primary AI model because it is, as of writing, by far the best tool we tested. That creates dependency. We have mitigated this deliberately: our context layer lives in Notion and BigQuery, and our agents are stored as structured text, not locked into a proprietary format. If we needed to switch models tomorrow, the knowledge layer and the agent logic would transfer. We are functionally LLM-agnostic at the infrastructure level, even if we are not at the execution level.

The second is data security. Giving an AI model access to your company's institutional knowledge creates genuinely new attack vectors and compliance questions that did not exist before. This is real and it is not trivial. I flag it here because any PE sponsor reading this should be asking about it, and any management team that hand-waves the question away is not taking the implementation seriously.

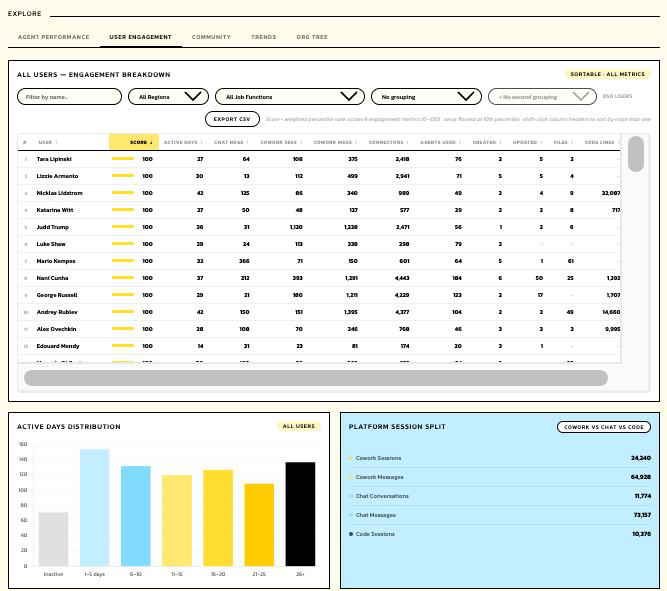

Tracking adoption: a dashboard didn't exist, so we built it in Claude Cowork

You cannot implement AI well if you do not know who is doing what. Most companies that deploy AI tools have no visibility into actual adoption. They know how many licenses they bought. They do not know who is using them, how deeply, or whether the usage is producing anything valuable. The standard vendor console tells you token counts and API calls. It does not tell you whether your paid search team is building agents or whether your client leadership function has connected AI to their actual workflow.

We built a custom tracking layer that sits on top of the AI platform and measures what matters: not just access, but engagement depth. Every employee gets a composite engagement score based on active days, session frequency, messages sent, connectors configured, agents used, code contributed, token efficiency and more. The dashboard is visible to leadership and to every employee, because community engagement drives adoption faster than any mandate. It took 2 afternoons and 72 rounds of feedback with Claude. The data below is real as at writing, with names anonymized. It covers 850 employees across 18 functions.

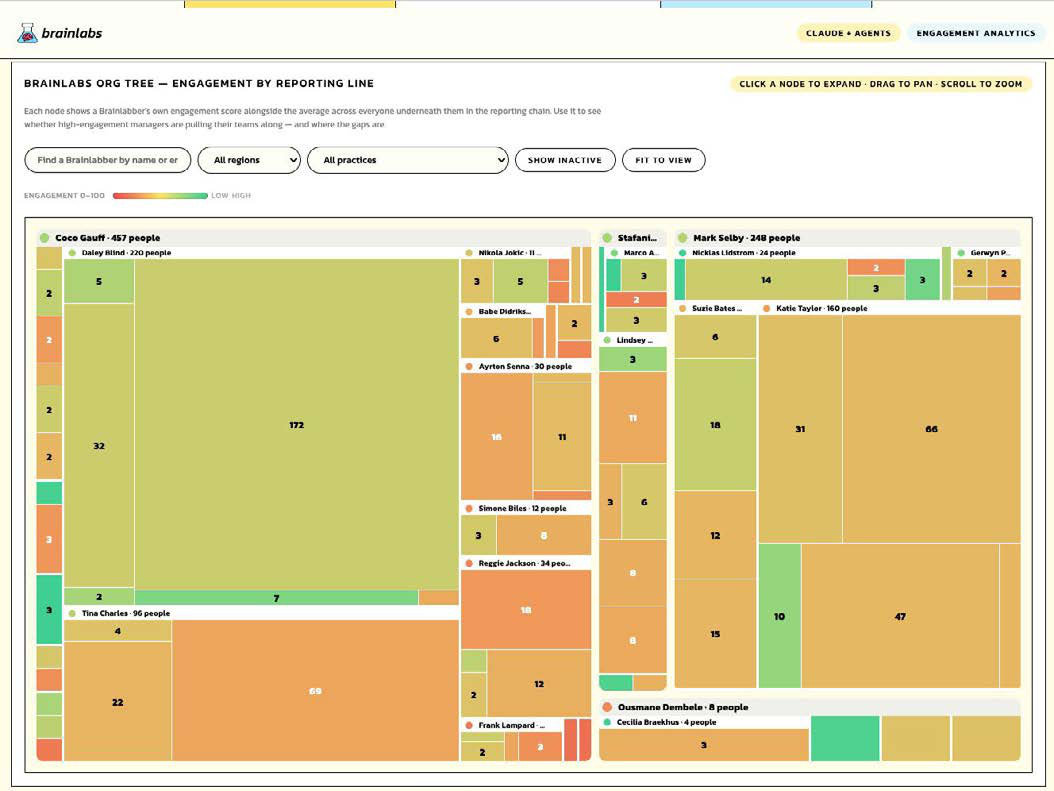

Engagement by function

Below is one of my favorite charts, a multi-layered treemap that lets us see which teams have high AI adoption and where we have gaps. Blocks are proportionate to team size and color denotes their engagement score.

This type of dashboard is the implementation data that PE sponsors should ask about. Not "do you use AI?" but "show me the dashboard. Show me adoption by function. Show me which teams are deep and which are developing. Show me the trend over time." If a company cannot produce this data, it does not know whether its AI investment is working.

Section 05b

The New Support Ecosystem

Billions in capital, thousands of forward-deployed engineers, and a new category of AI implementation firm.

Buy or Build is no longer the question

For a generation, the default question in enterprise technology was "buy or build?" Buy a SaaS product or build custom software. AI breaks that framing entirely. There is now a third option that did not exist before: Agents-as-a-Standalone-Service. I am calling this AaaSS. Partly because I am not a Consultancy so I can talk about AaaSS freely. And also because the industry has not settled on a name yet so I can make an AaaSS of myself in an otherwise very serious paper!

Billions will be spent on AaaSS. Entire industries will grow out of it. The old model was buying software licenses. SaaS gave you a product that did the same thing for every customer. The new model is agents that work for you, configured with your company's context, processes, and expertise. An agent that writes your client reports is not a software purchase. It is a hire that costs $0.05 per task, works around the clock, never forgets a process, and improves every time someone updates its instructions. Nick Bueno frames this as a fundamental shift: with agentic AI, you are building capacity, not buying point solutions. Agents require ongoing governance and performance management in ways that resemble talent management more than software procurement.12

This is neither technology nor pure services. Aaron Levie, CEO of Box, explains that AI is not a product you install and walk away from. It is a continuously evolving operational capability. The models change quarterly. A company that treats AI as a one-time software purchase will fall behind a company that treats it as a living system.13

What makes this model different from both SaaS and traditional consulting is the people who deliver it. The cool kids call this new breed "forward deployed engineers": practitioners who understand real business challenges and can build AI agents to solve them, or trained non-developers who can design, test, and improve agents. The skill set is new: part domain expert, part systems thinker, part builder. These people are hard to find because the role is new. But they are not hard to train, which matters more.

The growing AI implementation market

The biggest signal that AI implementation is a real market, not a consulting repackaging exercise, is who is putting capital behind it. Anthropic and OpenAI are both building enterprise services arms backed by billions in committed investment, staffed by forward-deployed engineers, and aimed squarely at mid-market companies — exactly the profile of most PE portfolio companies.

Anthropic launched its enterprise AI services capability with backing from Blackstone, Hellman & Friedman, Goldman Sachs, General Atlantic, Leonard Green, Apollo, GIC, and Sequoia — approximately $1.5 billion in committed capital. They created the Claude Partner Network with a $100 million dedicated fund and partnered with EPAM to build a force of over 10,000 Claude-certified architects, including 250 "Black Belt" forward-deployed engineers embedded directly in client businesses.

OpenAI took a different route. They formed the OpenAI Deployment Company with over $4 billion in initial investment, led by TPG alongside Advent, Bain Capital, and Brookfield. They acquired Tomoro, adding roughly 150 forward-deployed engineers, and built "Frontier Alliances" with Accenture, BCG, Capgemini, and McKinsey. Enterprise customers already represent over 40% of OpenAI's revenue.

This is billions of dollars from tier-one PE firms and the two leading AI model companies, all aimed at the same thesis: the models work, the implementation gap is the bottleneck, and whoever closes it captures the value. Both platforms are investing in forward-deployed engineers rather than traditional consulting partnerships. They understand that AI implementation is a building problem, not an advisory problem.

The opportunity for PE funds

The expertise that produces the results described in this paper is specific and nameable. It is not "AI strategy" or "digital transformation." It is the ability to do all of the following, together, inside a real operating company:

- Design and build the three-layer architecture (data, logic, execution) that makes AI agents work reliably at scale.

- Structure a company's institutional knowledge so AI can actually use it — the context layer that turns a generic model into one that knows your business.

- Build, test, and govern hundreds of production agents across every business function, from finance to client delivery to creative.

- Design the measurement infrastructure that proves whether any of it is working: adoption dashboards, ROI tracking, token economics.

- Run the change management that gets 779 out of 850 people actually using it, not just enrolled.

And right now, you cannot hire it in a conventional way. I have seen job postings asking for "5 years of Claude experience." Claude has barely existed for two years. No degree covers it and no consultancy has packaged it. The people who know how to do this learned by doing it.

I learned it myself. I had to. Two of the strongest contributors to our AI infrastructure came through the Brainlabs Academy: a graduate intake that received 5,399 applications in 2025, filtered to the 99th percentile on math and logic. These were not experienced AI engineers. They were smart people who learned fast because the work itself is the training. The entire capability took months to build, not years.

That is the opportunity for a PE fund. If a single company can build this in months with a small team, a fund can build the capability once and deploy it across every portfolio company. The context layer architecture, the dashboard, the skills library, the governance model, the measurement framework: all of it transfers. Prove it in one, deploy across ten. A standalone company running the same experiment gets a single data point. AI transformation that sticks is the kind of value creation that drives multiples at exit.

Section 06

The P&L and Valuation Impact

From token economics to enterprise value: how AI shows up on both sides of the ledger.

Tokenomics and cost management

Running AI agents at scale is not free. Every interaction with an AI model consumes tokens (the units of text that models process), and those tokens have a cost. At organizational scale, understanding and managing token economics is as important as managing any other operational cost line.

We have built an ROI calculator that tracks agent usage across the organization: which agents are used most, what they cost in tokens, how much time they save, and what the net return is per agent and per team. This turns AI from an opaque technology expense into a measurable operational investment with clear unit economics.

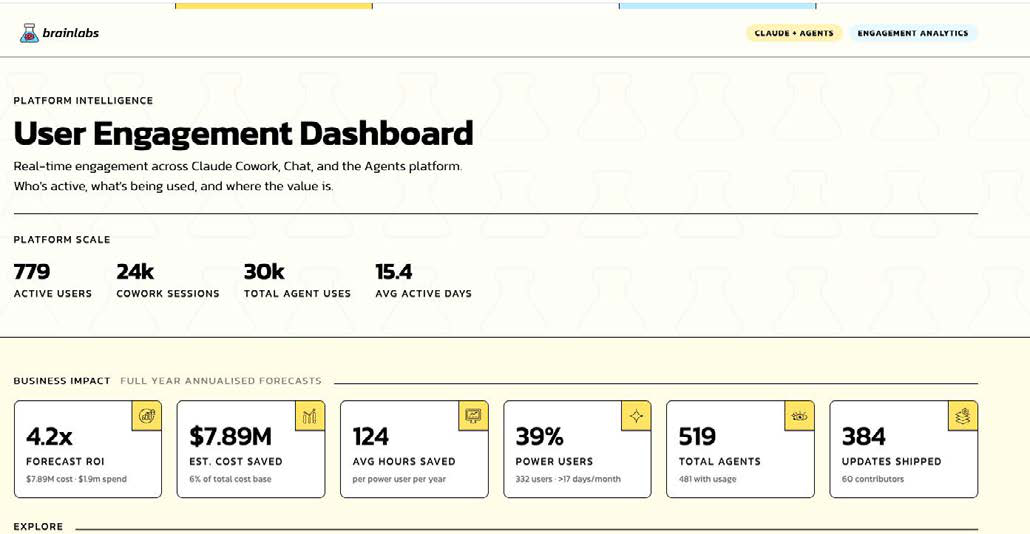

Across 850 approved users, 779 are active on the platform. At the time of writing, we've built 519 production agents, driven 30,340 total agent uses, with 63 individual contributors building agents for their teams. The top agents by usage tell you where the value concentrates: writing style enforcement (5,001 uses), presentation building (4,694), with action triage, branded deck creation, and email writing each exceeding a thousand uses.

A note on the cost figures: the dashboard tracks daily spend but this is accelerating at such a pace that we have turned this into an annual forecast. For Y1 this is expected to be $1.9M, around 1.5% of revenue. This is rather a lot for a new line item, but the unit economics still hold: we are tracking the time saved for every agent running and can use that to approximate $7.9M of work saved. The cost of tokens rarely outweighs the benefits of agentic automation.

Early Operating Data: Brainlabs AI Deployment

Full-cycle P&L impact data will follow in Q1 2027 as the first complete fiscal year of AI-native operations closes. The tooling matured too recently for anyone to report credible annualized results. But the operating metrics already tell a clear story about adoption, cost, and scale:

At single-digit cost per agent execution, with each execution replacing 30 to 90 minutes of knowledge worker time, the ROI on each use is measured in multiples. 779 of 850 approved users are active. 63 individual contributors are building agents for their teams. 183 users were active concurrently on peak day. This is not a pilot.

What happens to headcount?

Maybe AI will take all the jobs. Maybe it will not take any. Both sides of this debate are loud and neither is useful. The doomers say millions of jobs will disappear. The deniers say relax, it will never be as good as humans. Both camps are wrong.

The math is not as simple as "AI does 20% of the tasks, so you get 20% more output." Tasks are not equal. Some take five minutes, some take five hours. If AI handles the tasks that consumed most of the time (formatting, data gathering, first-draft writing), the capacity gain is disproportionately large relative to the number of tasks automated. In practice, we see AI absorbing 50–70% of the hours on work that represents a much smaller share of total task count.

The gain shows up as capacity: people doing more with the same team, or the same work with fewer people. For PE-backed companies focused on margin expansion during a hold period, the cost saving is real and available today. For companies in growth mode, the output multiplier is the better play. The right answer depends on the portfolio company's position and the GP's thesis.

Nick Bueno's bimodal distribution applies to individuals, not just companies. The performance gap between an account manager who uses AI to prepare for every client meeting and one who still does it manually is not 10%. It is 3x or 5x in output quality and speed. Over a hold period, that gap compounds into a fundamentally different workforce.12

A reality check: 93% of executives view AI as a cost reduction instrument within 18 months, but only 48% of targets are actually achieved, and just 25% report significant cost gains.8 The 30/70 split applies: 30% of the challenge is technology, 70% is organizational change.

Early evidence of P&L impact

The market is too young for anyone to claim definitive, audited results from AI-native operations. We are one of the first companies to deploy at this scale, and even for us, the first complete fiscal year closes in Q1 2027. But the early signals from BCG's cross-industry research are directionally clear: the top 5% of AI-mature companies are showing 1.7x the revenue growth, 3.6x the total shareholder returns, and 1.6x the EBIT margin of their peers.2 Those numbers should be treated with appropriate caution given how early the market is. But the direction of travel is consistent across every dataset we have seen, and it connects directly to how PE firms are starting to value these businesses.

The biggest fault line in PE valuations. Possibly ever.

There is no precedent for the spread that is opening up right now. Companies that moved on AI in 2024 and 2025 are building operational advantages every quarter. Companies that waited are watching the gap widen from the wrong side. In services businesses, where the operating model is built on people and process rather than physical assets, the divergence is already measurable. You want to be on the right side of this. Chadda is watching it happen:

"Within services businesses, the divergence is already measurable. Companies that shifted their delivery to AI agents have materially reduced headcount in operational roles. The businesses that moved early are pulling away. The ones that did not adapt have been left behind."

Sanjay ChaddaCanaccord GenuityChadda's observation aligns with what Canaccord Genuity is seeing across its M&A advisory pipeline. The firm ranks as the number one adviser in middle market US technology, media, marketing, and information services by deal volume.15 A review of its transaction activity over the past 24 months reveals a pronounced concentration of AI-native and AI-enabled deals across three categories:

Explicitly AI-focused transactions

- Kipi.ai — AI and data consulting, sold to WNS: 250+ proprietary accelerators, 450 data engineers and scientists.

- Applecart — $100M investment from Blackstone.

- Cuesta — sold to Riveron.

- EvoluteIQ — AI and hyperautomation, Baird Capital: native AI platform with Fortune 500 customers, proprietary Agentic Mesh Architecture.

- DeepIntent — $637M investment from Vitruvian Partners: proprietary platform unifying media, clinical data, and AI.

- Aktana — AI pharmaceutical engagement, sold to PharmaForceIQ.

Tech-enabled services and digital transformation

- NEORIS — $630M, digital transformation, sold to EPAM.

- Converge Technology Solutions — C$1.3B, IT solutions, sold to H.I.G. Capital.

- Quisitive — C$204M, Microsoft Cloud and AI, sold to H.I.G. Capital.

- Blankfactor — tech consulting, acquired by Globant.

- KMS Technology — digital engineering, Sunstone Partners.

- Analytics8, XponentL Data, Softcrylic — data and AI consulting specialists, sold to Boathouse Capital, Genpact, and Hexaware respectively.

Digital marketing and advertising technology

- Channel Factory — AI-powered contextual advertising, Truelink Capital.

- Veritone One — AI media agency, sold to Insignia Capital.

- Vistar Media — ~$600M, programmatic DOOH, sold to T-Mobile.

- Mars United Commerce and Dysrupt — sold to Publicis.

- Cardinal Digital Marketing — sold to Power Digital.

The pattern across all three categories is the same: AI capability has become a primary value driver in services M&A. Chadda personally advised on ten of these transactions. The multiples tell the story most clearly. The companies commanding premiums share specific characteristics beyond AI adoption. They have shifted from time-and-materials pricing to outcome-based models. They have built proprietary IP on top of third-party platforms, allowing them to realize higher gross margins atypical of traditional services businesses. And their management teams are actively using AI to disrupt their own operations before someone else does.

Section 07

Due Diligence

The questions that separate AI-ready portfolios from expensive experiments.

Before the detailed questions, use the AI Transformation Model as a diagnostic.10 Ask the management team: "Where are you on the curve?" If they say Level 1 (individuals using chatbots ad hoc), the transformation has not started. Level 2 means the foundation is being built. Level 3 (AI agents handling recurring workflows) is where measurable operational gains begin. Level 4 (AI as the system) is where compounding value kicks in. Most portfolio companies will be at Level 1. The best will be approaching Level 3. The ones to watch are the ones with a credible plan to get to Level 4 within the hold period.

Nick Bueno's shortcut is even simpler: ask the management team to show you something measured and real.12

"Show me something measured and real. Not a strategy slide. Not a vendor demo. A workflow that ran last week with AI doing the work, and the numbers behind it."

Nick BuenoManaging Director, Falfurrias Capital PartnersFor sponsors who want a rigorous, independent assessment, Crosslake, a Falfurrias-backed technology services firm, has built a dedicated AI Diligence practice drawing on over 6,000 transactions. They now treat AI readiness as a primary diligence category, not a subsection of the tech stack review.14 The six questions below are a starting point.

The six questions

These are not technology questions. They are value creation questions that happen to involve technology.

What percentage of your workforce has daily access to AI tools, and what percentage of those tools are integrated into core workflows?

Deloitte's data shows worker AI access expanded 50% in a single year, but only 25% of organizations have moved 40%+ of experiments to production.6 Access without integration is cost without value.

Can you name three AI deployments with measurable P&L impact, and what is the total financial value they've created?

Sixty percent of companies cannot define financial KPIs for AI.5 If the management team cannot answer this with specific numbers, the AI program is not connected to value creation.

Which jobs have been redesigned around AI, and what does the new workflow look like?

Eighty-four percent of organizations have not redesigned jobs around AI.6 If the answer is "none," the company is using AI as an add-on, not as an operating system change.

Who is the senior owner of AI, and does the CEO actively sponsor and back the initiative?

McKinsey's AI high performers are 3x more likely to have senior leader ownership.4 The right model is a senior owner who lives in the tools, with CEO sponsorship providing organizational authority and accountability.12

Is your institutional knowledge documented in a machine-readable format, or does it live in people's heads?

Without a structured context layer, every AI interaction starts from zero. AI-native companies make their knowledge accessible to both humans and machines.

What is your plan for agentic AI, and what governance framework exists for autonomous AI systems?

Seventy-four percent plan to deploy agentic AI within two years, but only 21% have governance in place.6 Sixty-seven percent are already considering autonomous agents.5 The technology is moving fast. Governance must keep pace.

Section 08

The Cost of Waiting

Every quarter of delay compounds against your exit multiple.

The data covered in Section 6 tells the story: the top 5% of AI adopters are pulling away on every metric PE cares about, while the majority derive no material value from AI at all.2 The adoption curve has split into two tracks. Companies are sorting themselves right now.

For PE, the relevant time horizon is the next exit, not 2045. If your hold period is five years, your portfolio companies need to be on the right side of this gap before you sell, not after.

The rate of improvement compounds this. AI task completion rates are doubling roughly every seven months.9 The difference between starting now and starting in a year is not twelve months of lost time. It is twelve months of accelerating advantage your competitors are building.

Bueno makes a related point about tempo: AI-native companies test, adjust, and redeploy on a weekly cadence. A portfolio company still running annual AI strategy reviews is playing a turn-based game while competitors move continuously.12

The technology exists. The economic evidence is in this paper. The companies that move now will widen their advantage every quarter. The ones that wait will pay more to close a wider gap.

So put AI transformation on the agenda at your next board meeting or portfolio review. Not as a technology item. As a value creation item. Bring this paper, pick one portfolio company, and run the 90-day proof of concept described in Section 5. You will have operating data before the following IC meeting.

GET ON WITH IT!

The opportunity is here and it is real.

About the Author

Daniel Gilbert is the Founder & CEO of Brainlabs, a 1,000-person media agency. Host of Show Me Your AI, covering tangible AI examples you can actually use at work. And author of the upcoming business book Don't Be a Midwit: How to Learn Good Judgement at Work So That AI Doesn't Replace You.

@DanGilbert · @danielgilbert1 · @ShowMeYourAi

Contributors: Nick Bueno, Managing Director, Falfurrias Capital Partners · Sanjay Chadda, Managing Director and Head of U.S. Technology Investment Banking, Canaccord Genuity.

Endnotes

- McKinsey Global Institute, The Economic Potential of Generative AI: The Next Productivity Frontier, June 2023.

- Boston Consulting Group, The Widening AI Value Gap, September 2025 (n=1,250 executives).

- McKinsey & Company / QuantumBlack, Seizing the Agentic AI Advantage, June 2025.

- McKinsey & Company, The State of AI 2025: Agents, Innovation, November 2025 (n=1,993 respondents).

- Boston Consulting Group, AI Radar 2025, January 2025 (n=1,803 executives).

- Deloitte, State of AI 2026, January 2026 (n=3,235 respondents).

- Boston Consulting Group, CEO's Guide to Maximizing Value from AI, July 2024.

- Boston Consulting Group, Driving Sustainable Cost Advantage with AI, May 2025.

- Matt Shumer, "Something Big Is Happening," February 2026. shumer.dev/something-big-is-happening

- Notion, The AI Transformation Model, 2026. Created in partnership with Ben Levick (Ramp), Geoffrey Litt (MIT/Notion), and others.

- Sanjay Chadda, Managing Director and Head of U.S. Technology Investment Banking, Canaccord Genuity. Interview with the author, May 2026. More than 300 sell-side transactions completed.

- Nick Bueno, Managing Director, Falfurrias Management Partners. Interviews with the author, May 2026.

- Aaron Levie, CEO of Box. LinkedIn post on AI deployment and forward deployed engineering, May 2026.

- Crosslake Technology Due Diligence. Crosslake runs a dedicated AI Diligence practice built on a dataset of over 6,000 transactions. crosslake.com

- PitchBook. Transaction totals represent US M&A / Control Transactions, All Buyout Types, and Growth/Expansion transactions <$500M in the Technology, Media & Telecommunications segment, LTM or 2023–2025.

Further Reading

- McKinsey & Company / McKinsey Global Institute, Technology Trends Outlook 2025, July 2025.

- Boston Consulting Group, Artificial General Intelligence Whitepaper, September 2024.

- Bain & Company, M&A Annual Report 2025, 2025.

- Bank of America, Consumer AI Usage Survey, 2025.

- Apollo Global Management, Private Market Secondaries Report, April 2026.

- Bain & Company, Global Private Markets Report 2026, 2026.

- Bain & Company, Technology Report 2025, 2025.

- Apollo Global Management, The Reset in Software PE, 2025.

- Blackstone, Office of the CIO: AI in Private Equity, 2026.

- PwC, Fearless Future: AI Investment Outlook, 2025.